Insight on Last Week’s News

- Aug 8, 2023

- 2 min read

What happened?

The US debt downgrade by Fitch Ratings from AAA to AA+ made headline news last week... Markets saw little impact. For reference and perspective, the S&P downgraded US debt from AAA to AA+ in August of 2011, right after that year's debt ceiling resolution.

What is the significance of an AA+ rating?

Although AAA is the highest rating, AA+ is still considered a very high "investment grade" rating from the rating agencies. The drop to AA+ does not place the country in danger but it does send a message.

Why did Fitch lower the rating?

Fitch cited three main reasons for the downgrade:

The expected fiscal deterioration over the next three years. The US government is expected to run a large budget deficit this year and next, which will increase the national debt.

Fitch is concerned about the recent political brinkmanship in Washington, which has led to repeated near-misses with default.

The high and growing general government debt burden. The US debt-to-GDP ratio is currently over 112%, which is well above the AAA median of 39.3%.

What do you need to know?

In the short term, the downgrade is unlikely to have any major impact on the US economy. For example, on the day of the downgrade, treasuries were actually up.

Rest assured, we will continue to monitor the rating agencies and the possible impact their decisions may have.

The reality is that the broader economy remains beyond our control. However, what you can control is the power to manage your budget, expenses, and commit to adhering to your long-term financial plan.

If you have any questions about the US debt downgrade, or anything else you have in mind, simply click reply to this message.

What else is happening in the markets and economy?

Global markets came under pressure last week for different reasons. Higher than expected inflation in the Eurozone led to anticipation of more rate hikes by the ECB while the Bank of England and Japan both tightened policy.

In the US, investors took profits in the lead up to the release of non-farm payroll data on Friday, as strong labor market numbers may potentially lead to further policy tightening by the Federal Reserve. Or, in the very least, keep rates higher for longer.

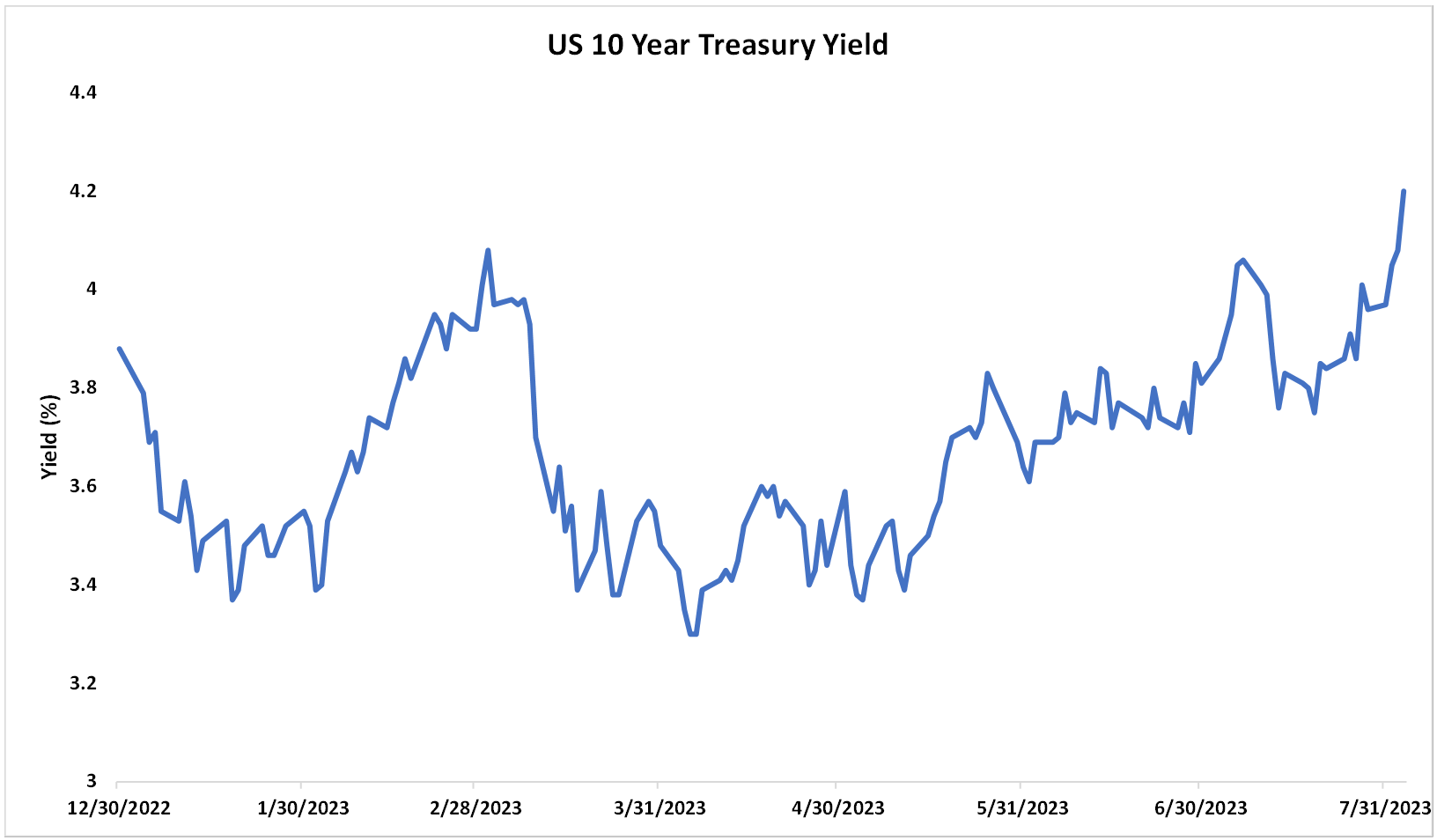

With mixed earnings reports from various companies and valuations that are back near 2021 highs, investors captured gains ahead of post earnings summer doldrums last week. ISM non-manufacturing new orders point to a service sector in the US that is still providing support for economic growth. Recent decreases in the probability of a recession are being confirmed by the long end of the US treasury curve (see chart below) as the yield on the 10-year treasury note moves to 2023 highs. CPI will be the focal point as the next confirmation opportunity for recent trends in inflation and for potential clues as to future policy action.

US 10 Year Yield Reaching New 2023 Highs Source: YCharts

Sources: Refinitiv, https://www.fitchratings.com

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Comments